PLTR

Conviction 4PLTR -- Combined Deep Dive Assessment

Date: 2026-03-02 Asset Class: Equity Ticker: PLTR (Palantir Technologies)

Fundamental Summary

| Metric | Value |

|---|---|

| Overall Score | 67.6/100 |

| Verdict | CAUTION |

Key Strengths: - Revenue growth 70% YoY (Q4 2025, accelerating); GAAP operating margin 40.9%; FY26 guidance $7.19B crushed consensus by 16% - Fortress balance sheet: $7.18B cash vs. $229M debt, current ratio 7.11x, FCF $2.1B TTM

Key Risks: - Extreme valuation: trailing P/E 209x, forward P/E 72x, P/S 70.5x -- 5-6x government IT peer median - Government concentration ~55% of revenue with DOGE uncertainty on ~40% of U.S. government contracts

(Full report: analysis/fundamentals/PLTR-synthesis.md)

Technical Summary

| Metric | Value |

|---|---|

| Overall Score | 5.5/10 |

| Bias | Neutral |

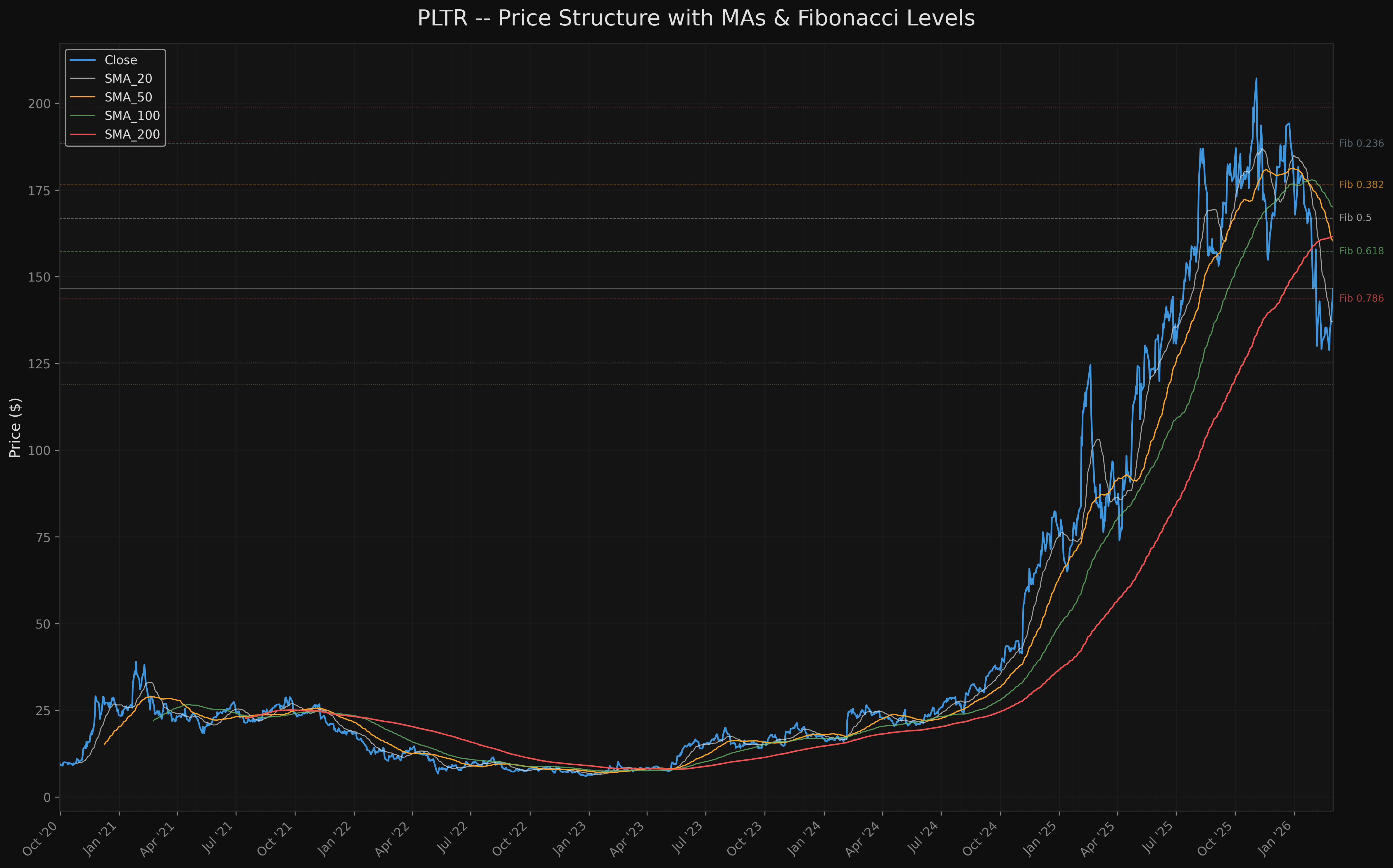

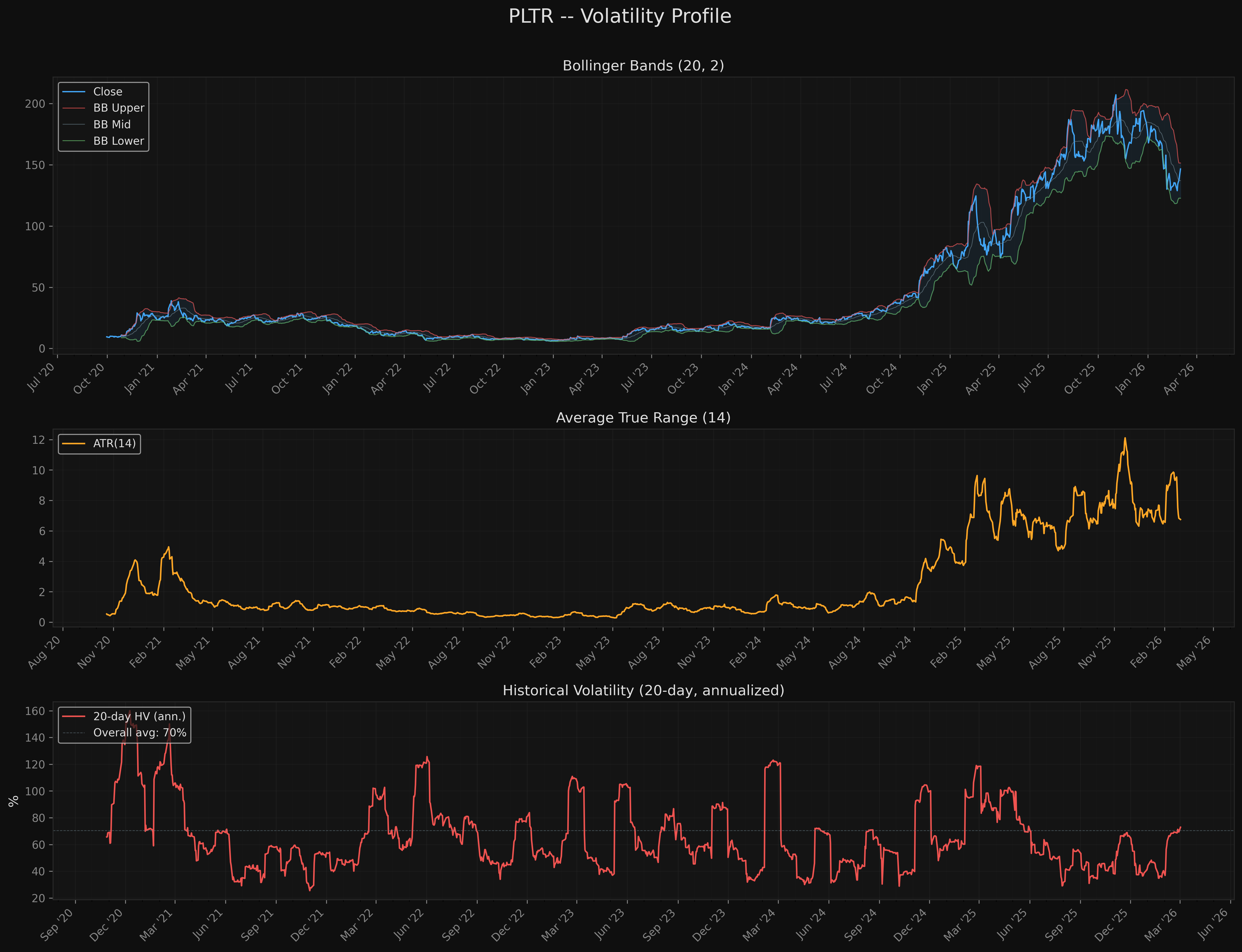

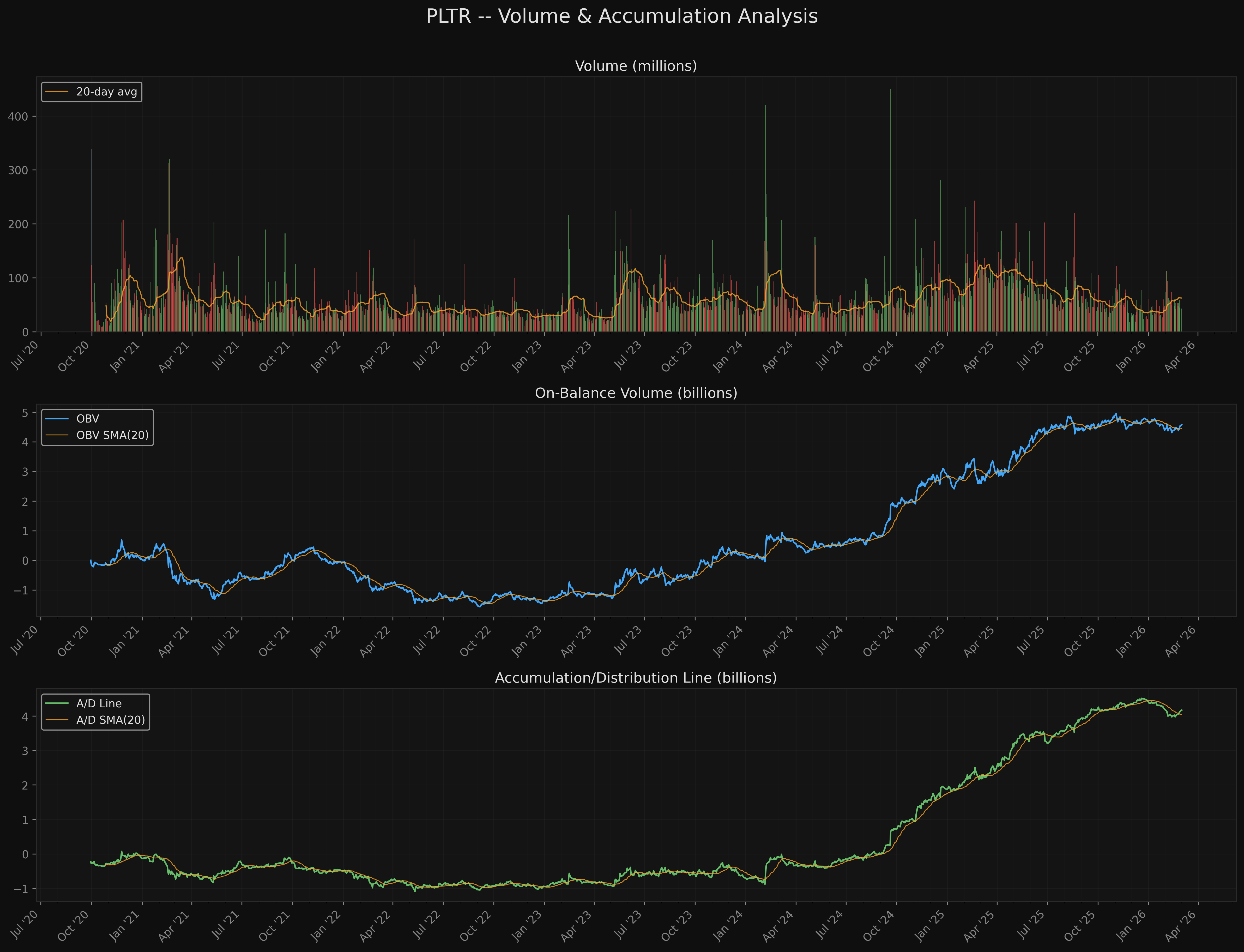

Trend: Death cross formed Feb 27 (SMA 50 below SMA 200); price below SMA 50/100/200 but above SMA 10/20. Momentum: RSI surging from 34.5 to 52.3 in 5 days; MACD bullish crossover; all three oscillators aligned. Key Levels: Support $126.23 (52wk low, double-tested), Resistance $153.27 (EMA 50), $160.25 (SMA 50).

(Full report: analysis/quant-research/PLTR-technical-2026-03-02.md)

AGREEMENT Assessment

Fundamental-Technical Alignment: PARTIAL AGREEMENT

Both analyses reach a cautious conclusion but through different lenses:

Where they align:

-

Both agree risk/reward at current levels ($146.57) is UNFAVORABLE for new entries. Fundamentals flag 72x forward P/E as inadequate risk/reward. Technicals show only 0.5:1 R:R at current price to first target.

-

Both agree the underlying business/asset has structural quality. Fundamentals: 92/100 earnings score, fortress balance sheet. Technicals: Wyckoff Spring reversal pattern with diminishing volume on retests.

-

Both identify attractive entry zones at LOWER prices. Fundamental bear case projects $70-90 on multiple compression; technical Zone 2 at $126-131 offers 3.7:1 R:R with a textbook Wyckoff reentry.

Where they diverge:

-

Fundamentals driven by VALUATION concern (72x P/E for a stock that hasn't missed earnings in 4 quarters). Technicals driven by TREND STRUCTURE concern (death cross, below major MAs). Different mechanisms, same conclusion: wait.

-

Fundamentals say the business is exceptional (92/100 earnings, 92/100 balance sheet) -- it is purely a price-paid problem. Technicals say the bottoming process is in early stages -- the Wyckoff Spring is promising but UNCONFIRMED (needs close above $150 on volume).

-

Fundamental 12-month base case: sideways to -10% as 70% growth normalizes and multiple compresses. Technical best case: recovery to $160-176 IF Spring confirms. These are not incompatible but operate on different timeframes.

Synthesis: This is a "great business, dangerous price" setup. The convergence point is patience -- wait for either technical confirmation (Spring validates above $150) or a pullback to entry zones where R:R becomes attractive. Do NOT chase the +16% bounce off the Feb low.

Key Levels

| Level | Price | Source |

|---|---|---|

| Resistance 2 | $176.47 | Fibonacci 0.618 retracement of $207.52-$126.23 decline |

| Resistance 1 | $160.25 | SMA 50 / death cross cluster |

| Current Price | $146.57 | -- |

| Support 1 (Zone 1) | $135-$140 | SMA 20 ($137.08) / consolidation zone |

| Support 2 (Zone 2) | $126-$131 | Wyckoff Spring zone / 52-week low area |

Risk/Reward Framework

Scenario 1: Zone 1 Entry (SMA 20 Pullback)

- Entry: $135-$140 (SMA 20 at $137.08 / consolidation zone)

- Target: $160.25 (SMA 50 / death cross cluster)

- Stop: $120 (below double-tested 52-week low with 5% buffer)

- R:R: 1.3:1 (to T1) / 2.2:1 (to T2)

- Probability: Moderate (requires pullback from current $146.57 level)

Scenario 2: Zone 2 Entry (Wyckoff Spring Retest)

- Entry: $126-$131 (retest of 52-week low area)

- Target: $160.25 (SMA 50 / death cross cluster)

- Stop: $120 (below double-tested 52-week low)

- R:R: 3.7:1 (to T1) / 6.8:1 (to T2 at $176.47)

- Probability: Lower (requires deeper pullback, but offers textbook Wyckoff reentry)

NOT RECOMMENDED: Entry at current price ($146.57). R:R to T1 is only 0.5:1 with $26.57 of risk to stop.

Conviction Assessment

| Component | Value | Rationale |

|---|---|---|

| Fund-Tech Agreement | 0.60 | Partial -- both cautious but through different lenses (valuation vs. trend structure) |

| Catalyst Density | 0.60 | Moderate -- Q1 2026 earnings, DOGE contract clarity, Spring confirmation at $150 |

| Data Quality | 0.90 | Large-cap with extensive coverage, full fundamental and technical data |

| Risk/Reward Asymmetry | 0.65 | Zone 1 offers 1.3:1 to T1; Zone 2 offers 3.7:1 to T1 |

| Red Flag Severity | 0.70 | All disclosed/structural -- extreme valuation, death cross, government concentration |

Conviction Score: 4 (Above Average) Weighted Score: 68.0/100 Position Sizing: 75% of target (4-5% of portfolio)

Note: Conviction 4 reflects analytical confidence and the quality of available entry zones -- NOT a recommendation to buy at current prices. The actionable framework below specifies WHERE to enter.

Actionable Framework

Position Type: New (Wait for Entry Zone) Position Size: 4-5% of portfolio at Zone 1; scale to 5-6% if Zone 2 triggers

Entry Zones: - Zone 1: $135-$140 | Trigger: Pullback to SMA 20 ($137.08) / consolidation zone. R:R to T2: 2.2:1 - Zone 2: $126-$131 | Trigger: Retest of Wyckoff Spring zone (52-week low area). R:R to T1: 3.7:1

Stop Loss: $120 | Below double-tested 52-week low ($126.23) with 5% buffer. A break below $126 negates the Wyckoff Spring thesis.

Targets: - Target 1: $160.25 | SMA 50 / death cross cluster -- first major overhead resistance - Target 2: $176.47 | Fibonacci 0.618 retracement of the $207.52-$126.23 decline

Key Monitoring Triggers:

Upgrade thesis if: - PLTR closes above $150 on volume >50M shares (Spring confirmation). Upgrades technical structure to 7.0/10, overall to ~5.8 Bullish. Consider Zone 1 entry. - Q1 2026 revenue beats $1.536B guidance AND government revenue shows sequential growth (DOGE concern cleared).

Downgrade thesis if: - PLTR fails to hold $140 after approaching $147-150 resistance zone (rally fading). Momentum downgrades to 5.5, structure to 4.0 -- overall drops to 4.7. - Q1 2026 government revenue declines sequentially (DOGE impact confirmed). Concentration risk is live.

Exit immediately if: - Close below $126 on elevated volume. This negates the Wyckoff Spring thesis entirely and projects a measured move to $100-110. No entry should be attempted. - Q1 earnings miss (revenue below $1.5B). At 72x forward P/E, a miss triggers severe repricing. Stand aside.

Limitations: - Fundamental analysis dated 2026-02-25 (4 days old). No material events since then, but PLTR price moved from ~$131 to $146.57 (+11.2%). Fundamental scores and valuation metrics are based on the lower price. - Technical analysis uses daily timeframe only. Intraday and weekly confirmation would strengthen the Wyckoff interpretation. - Wyckoff Spring is a subjective pattern identification. The "Spring" could alternatively be a brief pause before further decline if macro deteriorates. - Death cross reliability is mixed in research. This one formed after a -34% decline -- much of the damage may already be priced in. - PLTR's 70.5% annualized volatility and 1.97 beta mean position sizing must account for outsized daily moves. A 1-ATR stop requires absorbing 4.6% daily risk. - No insider buying identified at any price in 2025-2026. All insider transactions are pre-planned 10b5-1 sales.

Charts