ⓘ

[FORWARD-LOOKING RISK SIGNAL] Credit stress is the primary forward-looking indicator in the Signals system. Elevated readings (>50) correlate with deeper drawdowns over the next 1-3 weeks (Spearman rho = -0.23 with 21-day forward MDD).

⚠

Credit stress is high. Historically this correlates with materially worse forward outcomes. Reduce position sizes, tighten stops, raise cash.

Sub-Scores

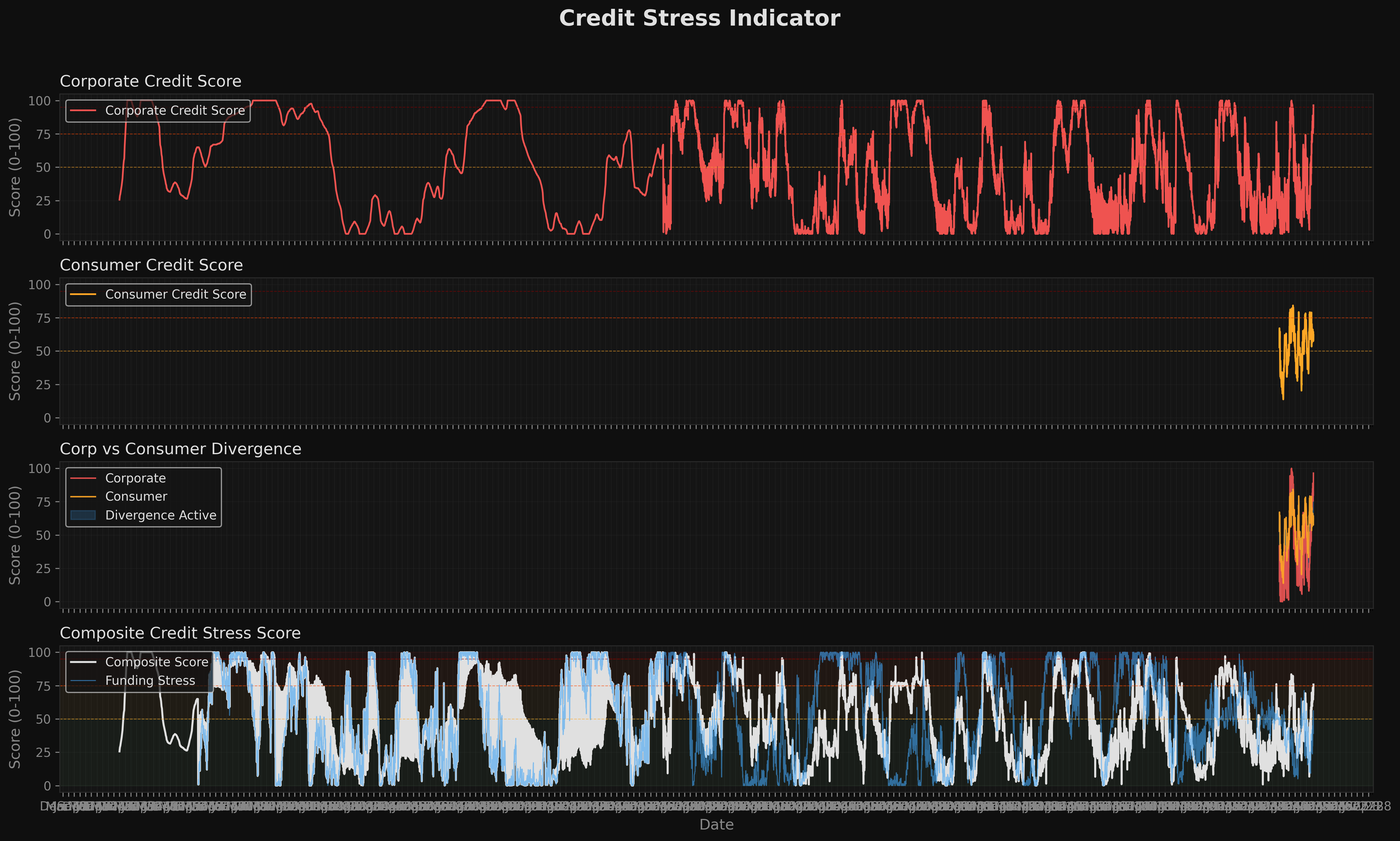

DIVERGENCE ACTIVE

Corporate Leads — Gap: 34.3 percentile points (corp=96.4, consumer=62.1)

NORMAL

ELEVATED

HIGH

CRITICAL

Composite Capitulation Score (CCS)

The CCS measures market-wide capitulation by combining four independent stress indicators. Each fires independently; 3-4 firing simultaneously marks historical bottoming zones.

✔

VIX z-score extreme (z=2.51):

Measures fear spike intensity. The VIX (CBOE Volatility Index) tracks expected 30-day S&P 500 volatility. A z-score compares today's VIX to its rolling 60-day mean/std.

Status: Triggers when z-score > 2.0 (current: 2.51). TRIGGERED -- VIX is spiking well above recent norms, indicating elevated fear.

✕

HYG drawdown (dd=-2.3%):

Measures credit market stress. HYG (iShares High Yield Corp Bond ETF) tracks junk bond prices. A drawdown from the 60-day rolling high signals investors fleeing credit risk.

Status: Triggers when drawdown exceeds -3% (current: -2.3%). NOT triggered -- high-yield bonds holding up.

✕

Breadth collapse:

Measures selling breadth. Tracks the ratio of down days in SPY over a rolling 10-day window. High ratios mean persistent, broad-based selling pressure.

Status: Triggers when 70%+ of the last 10 trading days are down days. NOT triggered -- selling pressure is not extreme.

✔

XLF below 200 DMA:

Measures financial sector health. XLF (Financial Select Sector SPDR) below its 200-day moving average signals structural weakness in banks and financials -- often a leading indicator of broader trouble.

Status: Triggers when XLF price is below its 200-day simple moving average. TRIGGERED -- financials are below their long-term trend, signaling structural weakness.

Data as of: 2026-03-27T16:00:00Z

Regime Context (SLOOS Quarterly)

DRTSCILM: +5.3% net tightening (2026-01-01)

Regime: Moderate Tightening

DRTSCLCC: +0.0% net tightening (2026-01-01)

Regime: Neutral

SLOOS data is quarterly. Values reflect bank lending standards, not incorporated into the daily composite score.

Private Credit Monitor

BDC Basket (ARCC, MAIN, PSEC, FSK):

20d Return: -6.07%

20d vs SPY: +1.24%

JBBB (B-BBB CLO ETF):

Drawdown from 60d: -2.11%

Private credit metrics are monitoring context only. They are NOT incorporated into the composite stress score.