Immune System

MARKET IMMUNE SYSTEM -- 2026-03-06

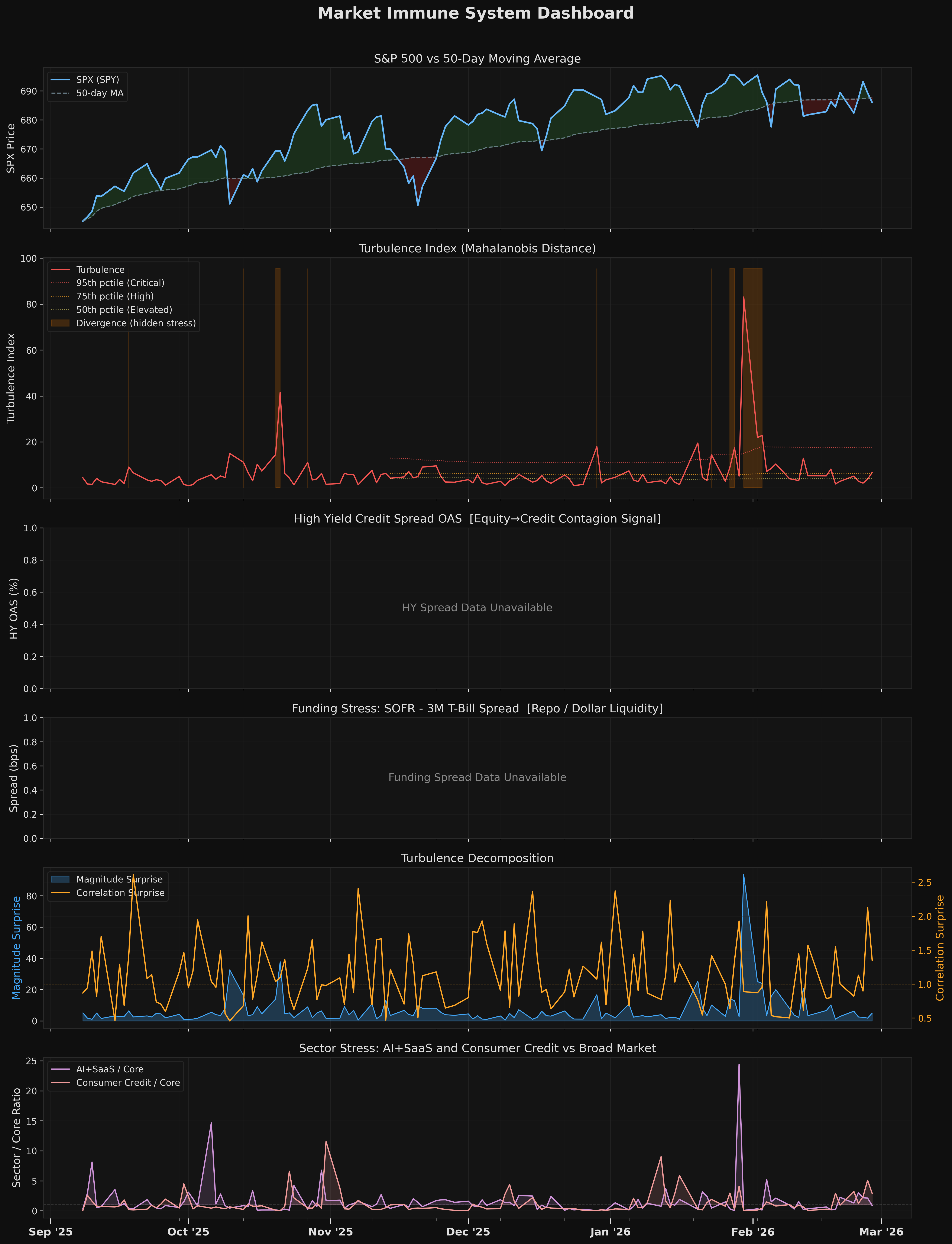

STATUS: HIGH Cross-asset turbulence is well above normal, indicating the market is in a stressed regime. Historically, high turbulence marks drawdown troughs more often than onsets (mean-reversion effect). Check the credit stress signal for forward risk assessment.

What's Driving It

- [CURRENT STATE] ⬆ Turbulence HIGH -- cross-asset stress well above normal

- [CURRENT STATE] ○ Dispersion NORMAL -- names moving in line with the index

- [CURRENT STATE] ○ Software NORMAL -- software stress in line with market

- [FORWARD-LOOK] ○ BKLN ABOVE 200-day MA -- leveraged loans stable

- [CURRENT STATE] ○ Breadth NEUTRAL -- balanced participation

INTERPRETATION

The market is in a highly stressed regime. Turbulence is high but this signal describes current conditions, not forward risk. Historically, high-turbulence periods show the strongest mean-reversion (best 21-day forward returns). However, if credit stress is also elevated, the combination has materially worse outcomes. Check credit stress.

RECOMMENDED ACTIONS (HIGH)

- Consider reducing position sizes

- Tighten trailing stops on all positions

- Raise cash allocation

- Monitor daily for escalation to Critical

Detailed Metrics

Turbulence: 19.8 (93th percentile) Magnitude Surprise: 20.5 Correlation Surprise: 0.96x Days Elevated: 2 days Divergence Active: NO Dispersion Ratio: 2.04 (66th percentile) Stealth Stress: NO Breadth (RSP/SPY): 1.01 (neutral) BKLN Trend: ABOVE 200-day MA

Sector Stress Ratios:

AI / Core: 0.13x

Software / Core: 0.17x

Consumer Credit / Core: 0.27x

Market Reference:

SPX: 672.38 (BELOW 50-day MA)

VIX: 29.49

Charts